The latest Auditor General’s report states that the state owned broadcaster, Fiji Broadcasting Corporation Limited may need some expert review of its business operations to identify areas that may need to be streamlined to reduce its business costs.

The 2014 report which has been tabled in parliament highlights that FBC has been incurring losses for the last four years - $516,943 loss in 2010, 1.137 million dollars loss in 2011, 7.1 million dollars loss in 2012 and 5.6 million dollars loss in 2013.

The Auditor General’s report states that the deficit of $342,887 for the shareholder’s equity in FBC’s Statement of Financial position indicate that the company does not have enough assets which stands at 22.4 million dollars to match all FBC’s borrowing to external parties totalling 22.7 million dollars.

The Auditor General said the major component of the liability is interest bearing borrowings of 19.4 million dollars in 2013 guaranteed by the government.

The audit said that the losses reported for FBC for the past four years demonstrate high operating costs incurred especially as the result of the expansion of the company into the television business and the company’s inability to generate adequate revenue in addition to the government contribution to finance its business costs.

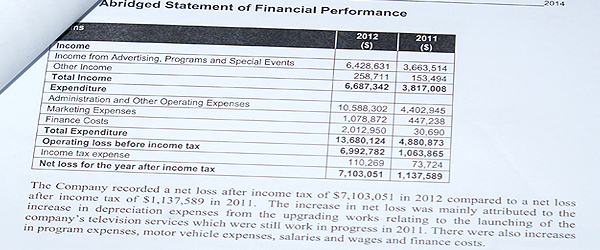

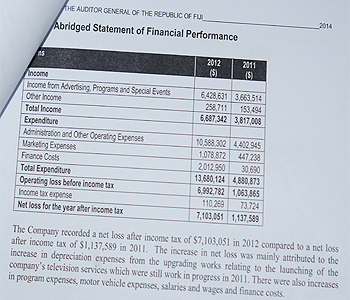

Meanwhile the audit said FBC’s recorded a net loss of 7.1 million dollars in 2012 compared to a net loss of 1.13 million dollars in 2011.

This was mainly attributed to the increase in depreciation expenses from the upgrading works relating to the launch of the company’s TV services which were still in progress in 2011. There were also increases in program expenses, motor vehicle expenses, salaries and wages and finance costs.

The 2013 net loss was 5.6 million dollars.

Total expenditure for the state owned broadcaster in 2012 was 13.6 million dollars while the expenditure for 2013 was 14 million dollars.

The total income was 6.6 million dollars in 2012 and 8.4 million dollars in 2013.

It has also been noted that the company accounts for all government grants received after 1st January 2010 as capital contribution. This is a departure from International Accounting Standards accounting for government grants provided to compensate the company for expenses incurred to be recognized in profit or loss as other income on a systematic basis in the same period that the expenses are recognized.